10 Steps to Smart Grids

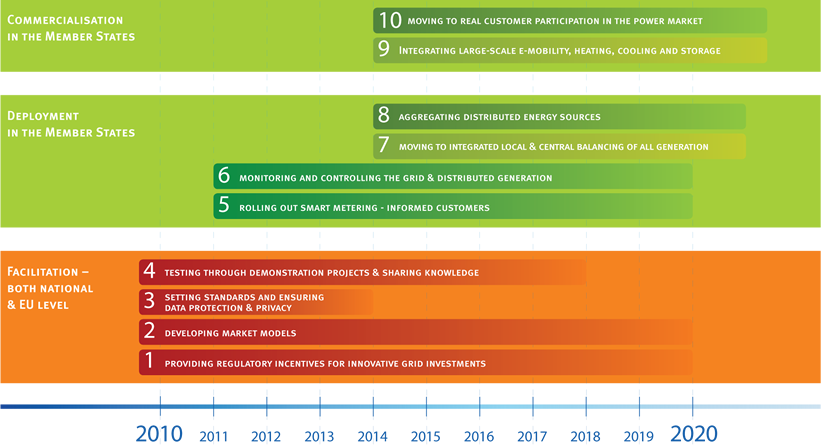

Smart grids will not be rolled out in a single swoop. Instead, their implementation is an incremental and continuous step-by-step learning process, characterised by different starting points throughout Europe. Smart grids are not an instant revolution, but a steady evolution which has to include the customer as well as energy suppliers and producers. We believe that there is a great need for more awareness about what the deployment of smart grids will include, in particular with a view to identifying the most important steps for policymakers and industry. To support the transition from the traditional to the new flexible power system, this paper develops an indicative EU roadmap for the deployment of smart grids within the next 10 years. Our 10 steps point out what we today see as milestones on the way towards new commercial customer-oriented solutions which will contribute to a successful EU energy policy in terms of sustainability, security of supply and competitiveness. While the facilitation phase (our first four steps) will require EU support, the following deployment and large-scale commercialisation will take place in those member states where smart grids are considered to be economically viable, taking into account the energy supply mix, current and future demand, and the status of networks.